May I be the first to admit this report reads long.

For those readers who prefer an executive summary to the analytical equivalent of War and Peace, the “At a Glance” summary below may suffice. For those who want to understand the rhyme and reason behind how the future of any asset classes’ returns are at least somewhat dependent on how they have been performing over the previous 5 years, then this report should provide the analysis and information that you are seeking.

We will end our report with the compelling reasons for sticking with a truly diversified asset allocation model that covers multiple asset classes both private and public.

At a Glance:

- Mean reversion is the tendency of asset classes to move back toward their long-term average returns after extended periods of strong or weak performance.

- When markets correct, they often overshoot, much like a pendulum, amplifying volatility and testing investor behaviour.

- Historical data across public equities, private markets, real estate, infrastructure, and bonds shows a consistent pattern.

- Periods of exceptional performance are often followed by muted or negative returns.

- Periods of poor performance tend to create the conditions for strong recoveries.

- Today, many public equity markets are trading at or near record valuations, increasing the risk of future mean reversion.

- By contrast, several private asset classes, including real estate and infrastructure, are emerging from below-average return environments, where mean reversion may work in investors’ favour.

- A disciplined, diversified asset allocation, grounded in both public and private markets, can reduce volatility and improve long-term outcomes.

- This is the foundation of our Core approach, designed to compound wealth over full market cycles rather than chase short-term performance.

For decades, landing on the cover of Sports Illustrated has marked a turning point for many athletes. Not because of superstition, but because the history is hard to ignore. An internal review of more than 2,400 Sports Illustrated covers found that many featured athletes experienced a noticeable decline in their performance shortly after.

The reason is simple: Athletes earn that spotlight because they are performing at exceptional levels. But extremes rarely last. When performance stretches well beyond what is deemed typical, the forces that created those highs tend to fade, and results often drift back toward more familiar territory.

Markets are no different. Periods of unusually strong returns often cluster near peaks, just as periods of weak performance tend to appear near troughs. Over time, returns have historically tended to move back toward their long-term average. This dynamic is known as mean reversion. It does not predict what will happen next, but it helps explain why markets do not remain at extremes indefinitely. What’s happening in both cases is the same underlying pattern. To understand it more clearly, it helps to start with what we mean by “mean reversion.”

What Do We Mean by Mean Reversion

If one looks up the definition of the word mean, you will find several possibilities. It could represent a lack of understanding, as in “I don’t know what you mean,” or convey a level of importance, such as “this means a lot to me”.

In the case of mean reversion, the definition is a mathematical one. “Mean” refers to the average of a series of data points, and “mean reversion” refers to the tendency of asset classes to revert to that mean or average after extended periods of time of overperformance or underperformance. For the purposes of this discussion, let’s assume five-year periods of over- or under-achievement.

How does this apply to mean reversion? When asset classes correct from new highs and lows, they do not simply return to their average. Much like a pendulum, they are prone to overcompensate on the way back.

This, in turn, tends to exacerbate negative human behaviour, leading to underperformance.

Why Mean Reversion Deserves Attention

We are used to seeing volatility in public markets, particularly in stocks. But it exists in all asset classes to varying degrees. In some cases, the difference in annual returns between one five-year period and the next can reach as high as 30. That is not a typo.

The purpose of this article is twofold. First, to provide a perspective on how mean reversion can impact returns, volatility, and behaviour.

Second, to review our asset allocation model, which we refer to as Core, and show how it is designed to outperform over medium- to long-term periods with much less sensitivity to mean reversion than traditional models. While the theory behind Core is the same as that used by Canada’s largest pension plans, which are considered world-class asset managers known as the Maple 8, it will underperform a traditional 60/40 portfolio from time to time, as it has over for the last two years.

We believe that over reasonable time frames, Core will outperform public balanced models as public asset classes mean revert from their very lofty positions.

Our objective is to help ensure that the journey to achieve and maintain wealth and financial independence does not feel like travelling the road below.

Looking at the Data

In our analysis, we examined eight asset classes and indices: the S&P 500, S&P/TSX, Cambridge Private Credit, Cambridge Real Estate, Cambridge Infrastructure, Cambridge Private Equity, the Markit iBoxx Liquid High Yield Index, and the Bloomberg Aggregate U.S. Bond Index.

For each, we identified the best-performing five-year periods over the past 90 years (where data was available) and selected the top five of those periods. We then compared those results with the five-year period that immediately followed each peak.

We also examined mean reversion by looking at periods when these asset classes performed poorly over five-year stretches and then comparing those results with the five-year period that immediately followed.

Let’s examine each data set separately, starting with the S&P 500.

U.S. Equities: S&P 500

S&P 500 Equal Weight Total Return

Canadian Equities: S&P/TSX Composite Total Return

Cambridge Private Credit

Impact of Closed-End vs Open-End Funds on Liquidity

Cambridge Real Estate

Cambridge Private Equity

Cambridge Infrastructure

Bonds: Even the “safe haven” Mean-Reverts

Performance Summary & Calendar Year Net Returns

Why Private Assets at All?

Private Fixed Income

Private Equity

Real Estate

Core: Putting It All Together

Summary

U.S. Equities: S&P 500

S&P 500 Ann. Return (1926 - 2025): 10.49%

What can we observe from these results?

- The average five-year peak returns are almost 19% per year higher than the returns in the five years that follow. In two cases, the gap is closer to 30% per year.

- The mean total return (average) for the S&P 500 was 10.49% from 1926 to 2025.

- Over the last five years, the S&P 500 total return to January 6 was 13.5%, or about 3% above the long-term average. That is not excessive. However, when we look at the last three years, the S&P 500 total return has been 23.6% annually, roughly in line with the high-performance group.

This raises the question of whether U.S. stocks can extend the bull market for another two years. As a note of caution, consider the graph below showing the Shiller CAPE index, which measures the S&P 500’s 10-year trailing P/E ratio. Valuations are near record levels and roughly one-third higher than they were in 1929.

Shiller PE Ratio

Source: Robert J. Shiller, Irrational Exuberance (Cyclically Adjusted P/E Ratio for the S&P 500), via multpl.com.

If this bull market continues, our equity strategy will underperform as we become more defensive, focusing on dividend cash flow rather than the Magnificent Seven.

We will not be alone. The chart below shows the equal-weighted S&P 500 total return over the past three years. By reducing the influence of technology stocks and AI-driven names, it provides a useful contrast. Over this period, the index has still delivered a very respectable 12.1% annually, but that is roughly 10% per year less than the S&P 500 total return index.

Let’s hope that when the S&P 500 does revert, it does so without being “unkind, cruel, or malicious,” as was the case in Mean Girls.

S&P 500 Equal Weight Total Return (^SPXEWTR)

USD | Jan 14, 20:00

Source: YCharts, S&P 500 Equal Weight Total Return Index (SPXEWTR).

Canadian Equities: S&P/TSX Composite Total Return

S&P/TSX Composite Ann. Return (1956 - 2025) 9.43%

Results for the TSX are currently less extreme with respect to valuation than they are for the S&P 500, but they are still quite elevated.

- The gap between the best five-year performance and the ensuing five years is more than 20% annually.

- The long-term return for the S&P/TSX Composite total return has been just over 9% per year since 1960.

- However, over the last five years, returns have been approximately 18% annually or roughly double their historical average.

- This has reduced the dividend yield on the index to just under 2.5% annually.

More than a year ago, we decided to focus on dividend growth stocks for the Canadian market. As a result, our Canadian Equity Fund now has a current yield of approximately 3.75%, or about 50% higher than the index. That shift has reduced total returns to an average of 12.8% over the last five years, but with a significantly lower level of volatility.

It is equally important to note that the average of the five worst-performing periods for the S&P/TSX is close to zero, followed by average returns of more than 16% per year.

Private Markets: Smoother in Practice, but Not Immune

Cambridge Private Credit

Cambridge Associates has been advising major institutions with respect to asset mix since 1973. They maintain indices for private credit, real estate, and infrastructure. We begin with private credit.

In the case of fixed income asset classes, we would expect a smaller gap between over- and under-performing periods of time. Nevertheless, the change is still quite notable, exceeding 10% per year, even though changes in actual interest rates over these periods were more modest. Private credit is more impacted by the direction of interest rates, with rising rates presenting challenges, and by recessionary environments when default rates rise.

Average annualized return from Apr 1986 to Mar 2024: 9.83%

Average return for most recent 5yrs (Apr 2019 to Mar 2024): 8.54%

One interesting point to note about private credit is that, over long cycles, it has delivered returns comparable to equity markets with much lower volatility. Liquidity for private credit has limitations, but they are notably less restrictive than what investors experience in private equity or real estate.

Impact of Closed-End vs Open-End Funds on Liquidity

Most private asset funds, whether credit, equity, or infrastructure, are closed-end. This means an investor commits a certain amount of capital to a particular asset class. For example, assume a commitment of $1 million. That capital is invested by the asset manager (the general partner) over a period that typically spans three to five years. The investment then remains in a limited partnership until the individual assets within the partnership are sold.

The full process often takes 10 to 15 years before an investor receives both their capital and returns.

Returns are often higher than in public markets, particularly in private credit, and in cases such as infrastructure there are few public alternatives available.

Returns to investors are measured based on when capital is invested, not when it is committed. This has a tendency to exaggerate returns when compared with open-ended evergreen vehicles, where all capital is invested at one time. For a more detailed explanation of these two structures, see the appendix below. In some comparisons, a return of 9% per year in an open-ended fund can deliver the same dollar outcome as a 14% per year return in a closed-end fund.

This makes comparisons difficult. For context, the five-year annualized return of the Nicola Private Debt Fund (open-ended evergreen pool) was 8.7% as of November 30, 2025.

Cambridge Real Estate

The table below shows absolute returns for commercial real estate in North America over the past several decades. Most investors are aware of how poorly both commercial and residential real estate markets have performed over the last three years. Historically, the total return for income-producing real estate has closely matched stock market returns, including dividends.

Since 2022, those relationships have been turned on their head. The question is whether we are likely to see mean reversion between these two asset classes.

Real Estate Ann. Return (Q1 1986 - Q1 2024) 7.78%

The table shows the extreme shift in returns between the five years leading up to the Global Financial Crisis and the five years that followed. The gap was almost 30% annually.

How do things look today? There are two charts below. The first shows the MSCI Private Commercial Real Estate Index for Canadian institutional investors such as us.

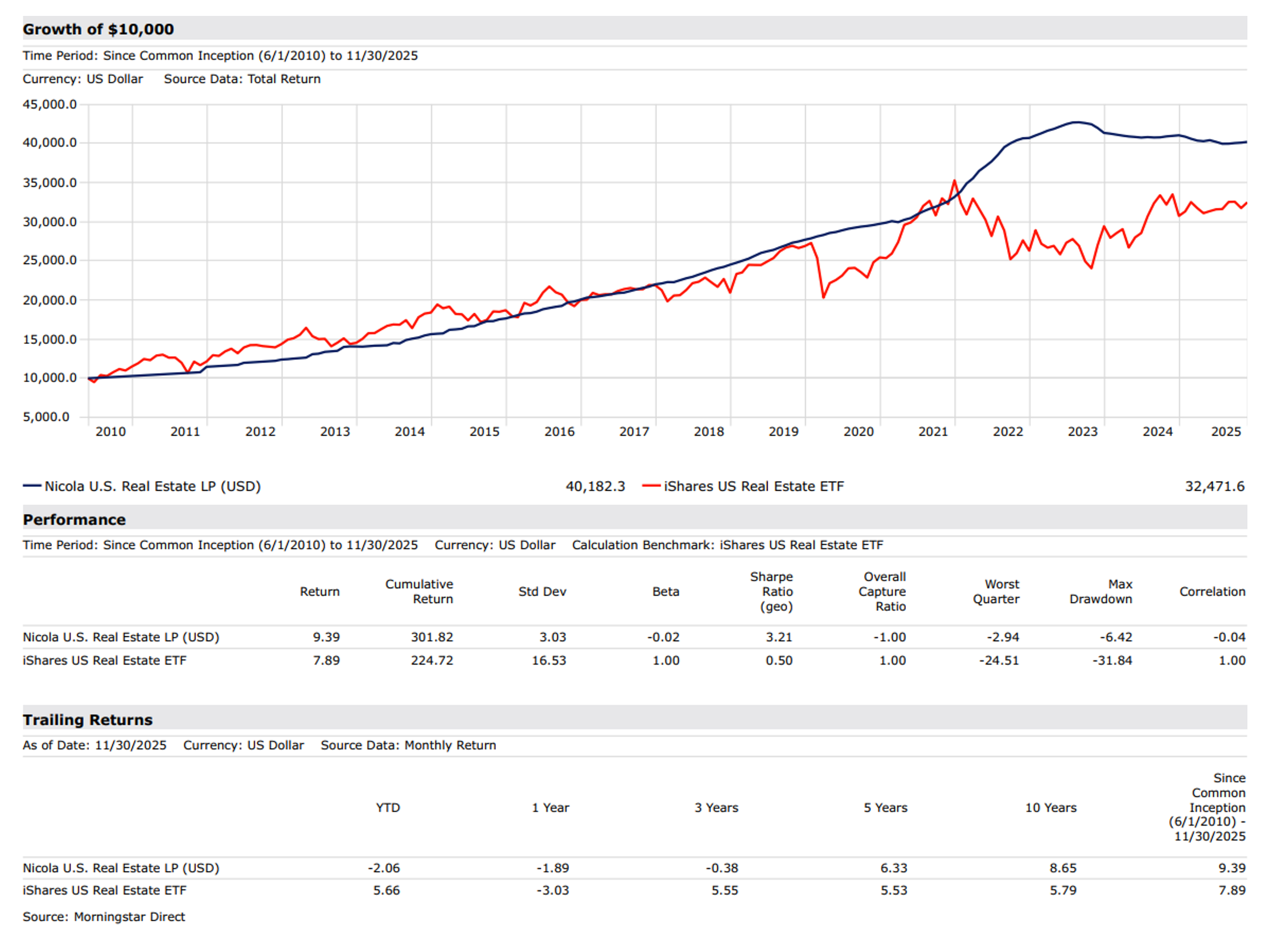

Note that returns since 2022 have been negative for the index but positive for Nicola Canadian Real Estate LP, with a spread of 3.2% per year. Over a five-year period, returns improve to 4.2% and 7.4%, respectively. Both the index and our Canadian real estate funds are private. REITs represent the public version of real estate investing, and both their long- and short-term results have been disappointing.

The chart below shows the five-year total return for the S&P/TSX Capped REIT Index. On a cumulative basis, the index delivered approximately 28% (about 5% annualized), compared with more than 40% cumulative (about 7% annualized) for the Nicola Canadian Real Estate LP. The chart also highlights the level of volatility experienced by the index.

S&P/TSX Capped REIT

Source: S&P Dow Jones Indices, S&P/TSX Capped REIT Index Total Return, via S&P Global.

Looking over the longer term in both the U.S. and Canada, and comparing our private approach to real estate investing, it is clear why we view privately owned real estate, run by strong management teams, as the better model based on both return and risk.

Nicola Canadian Real Estate LP vs. iShares S&P/TSX Capped REIT ETF

Nicola U.S. Real Estate LP (USD) vs. iShares U.S. Real Estate ETF

Cambridge Private Equity

Private equity returns are represented using the Cambridge Private Equity Index, a commonly used institutional benchmark.

Private equity has delivered strong long-term returns, but results have been cyclical. Periods of very strong performance have often been followed by more moderate outcomes, while weaker periods have tended to be followed by meaningful recoveries.

The table below highlights a clear pattern of mean reversion. The best five rolling five-year periods generated average annual returns of 23.6% but were followed by much lower returns averaging only 9.6%. By comparison, the weakest five-year periods generated average returns of 6.7% yet were followed by strong rebounds averaging 16.9% per year over the next five years.

Private Equity Ann. Return (Q4 1983 - Q1 2025) 13.38%

Cambridge Infrastructure

Infrastructure has been available to major institutions for many years. It tends to provide strong cash flows that are often inflation-protected, but it also requires long commitments of capital, as assets such as toll roads, hospitals, bridges, and tunnels have lifespans measured in decades. Infrastructure also benefits from tax-favoured cash flow and a low risk of default, given that tenants are often governments or government-related entities.

Notwithstanding these characteristics, infrastructure can still mean revert. In the five years leading up to the Global Financial Crisis, returns averaged more than 17% annually. In the five years that followed, returns dropped to approximately 2% per year. In most cases, cash flows would have remained relatively stable. The impact came from pricing.

Infrastructure Ann. Return (Oct 1994 - Mar 2024) 5.0%

Infrastructure Ann. Return recent 5-year (Apr 2019 - Mar 2024) 10.2%

Infrastructure Ann. Return recent 5-year (Apr 2015 - Mar 2024) 10.1%

Bonds: Even the “safe haven” Mean-Reverts

Bloomberg U.S. Aggregate Bond Total Return

Bonds are supposed to be the safe haven in a 60/40 portfolio of stocks and bonds, but there are many instances where mean reversion reveals its more brutish and ugly nature.

The table below shows the impact of the sharp decline in interest rates after Paul Volcker pushed them to more than 20% by 1981. That rise and subsequent fall in rates ultimately succeeded in bringing inflation under control, but at the cost of mortgage rates reaching as high as 24% for those unlucky enough to be on the wrong maturity date.

It was a home run for investors in long bonds, who earned almost 20% per year over the following five years. While the next five years still delivered reasonable results, with average total returns of about 9%, returns declined by roughly 10% per year from the prior period. That bond bull market continued until COVID drove 10-year yields down to 0.5% in early 2022.

Bloomberg US Aggregate Bond Ann. Return 1976-2025: 6.52%

A similar pattern of mean reversion shows up in high-yield credit markets, as seen in the Markit iBoxx Liquid High Yield Index. The strongest five-year periods for high-yield bonds averaged just over 10% per year but were followed by much lower returns averaging about 5.7%.

By contrast, the weakest five-year periods produced average returns of only 1.5% yet were followed by strong recoveries averaging more than 7% per year over the next five years.

Even in higher-yield segments of the bond market, periods of strong performance tend to set the stage for more muted returns, while periods of stress often create the conditions for stronger recoveries.

Markit iBoxx Liquid High Yield Ann. Return (1999 - 2025) 5.20%

Since that time, holders of 10-year U.S. Treasuries have lost more than 2% per year of their capital, even after taking into account the interest they earned.

Source: S&P Dow Jones Indices, S&P U.S. Treasury Bond Current 10-Year Index Total Return, via S&P Global.

We were very concerned about the record lows reached by 10-year yields in 2020, and we made a major change in how we invested in bonds, particularly with respect to duration.

The table below illustrates the significant outperformance our clients have experienced in the Nicola Bond Fund compared with what the broader markets were offering (performance as of November 30, 2025).

Performance Summary

Calendar Year Net Returns

The gap between our approach and the U.S. Total Return Bond Index was more than 7% per year over the last five years. The radical choices investors made during the early days of COVID, and the flight to the perceived safety of U.S. Treasuries, laid the groundwork for the mean reversion in bond returns that followed.

We would argue that because all asset classes are subject to periods of heightened volatility driven by mean reversion, only a disciplined and proven asset allocation model can help minimize the damage these price swings inflict on investors.

Strategic Asset Allocation

If we look at historical returns across asset classes over more than 100 years, several patterns emerge.

- The total return from global public equities, including dividends, has generally ranged from about 8.5% to 10% per year, with U.S. markets at the higher end of that range and Canada just under 9%.

- The return from government bonds has averaged 4.5% to 5% over the last century. Higher returns can be earned by moving up the risk ladder for lending with commercial loans, mortgages and private credit but only the latter has exhibited stock-like returns over decades

- According to an extensive NBER study published in 2017, income-producing real estate has matched total stock market returns with lower volatility. The study examined 145 years of data across 16 countries.

Estimates from major consulting firms suggest that global financial assets total between $450 trillion and $600 trillion USD. These figures exclude personal residential housing, which alone is estimated to be worth more than $250 trillion USD as of 2025. Approximately 55% of global investable assets are allocated to public equity and bond markets. That implies that other asset classes such as commercial real estate, private companies, infrastructure, private debt, and commodities represent nearly $250 trillion USD.

Outside of personal homes and recreational properties, most individuals hold most of their investments in publicly traded stocks and bonds. Private asset markets are often difficult to access for several reasons.

- First, private investments typically require significantly larger capital commitments than those needed to invest in stocks or bonds directly, or through mutual funds and ETFs.

- Second, while mutual funds and ETFs may hold dozens or even hundreds of securities, private equity and private credit funds often invest in only 10 to 15 positions. Achieving proper diversification requires commitments to multiple funds.

- Third, liquidity is limited. Closed-end structures, which are common in private equity and private credit, can lock up capital for 10 to 15 years before all funds are returned to investors.

- Real estate exposure can be obtained through publicly traded REITs, but returns have historically lagged private real estate investment pools and with significantly higher volatility. This can be seen by comparing our Canadian and U.S. private real estate pools with publicly available REIT indices, as discussed earlier.

- Finally, investors in private real estate funds cannot easily sell their interests to other investors. Liquidity is typically requested by tendering units back to the fund itself. To meet redemptions, a fund may need to sell assets, bring in new investors, or rely on credit facilities. This process can take several months, and in periods of stress, potentially years if many investors are seeking liquidity at the same time.

Why Private Assets at All?

Given the issues and limitations noted above, why would an investor include private assets in their portfolio?

Here is why:

- Liquidity needs are often limited. Large investors such as major pension plans, endowments, and sovereign wealth funds do not have significant liquidity needs that require their portfolios to be convertible to cash within days. The same is often true for individual investors, yet many still pay a premium for liquidity they rarely, if ever, need.

- Private assets represent a large portion of investable assets. Private assets account for close to 50% of the world’s investable assets. Including them in a portfolio creates diversification and reduces volatility. A useful comparison is the Canada Pension Plan, with assets of approximately $777 billion CAD as of late 2025, and Norway’s $2 trillion USD sovereign wealth fund, managed by Norges Bank Investment Management. Over the ten years to September 2025, Norway’s fund returned 6.7% per year, compared with 8.8% for the Canada Pension Plan. Norway’s portfolio is roughly 70% invested in public equities and almost 30% in bonds, with less than 2% allocated to private assets. By contrast, the Canada Pension Plan held approximately 29% in public equities, 15% in bonds, and 56% in private equity, credit, infrastructure, and real estate. The result, even after a strong recent bull market for public stocks, has been a return advantage of roughly 2% per year with lower volatility.

- Investment managers can be more actively involved. Managers of private capital can play a more active role in how underlying assets perform. In private companies, this may include board participation or helping to recruit and develop senior management. In real estate, long-term results are driven by leasing decisions, financing structures, and value-added development. In most cases, manager compensation is directly tied to achieving specific return targets for passive investors.

- Endowments and pension plans allocate meaningfully to private assets. Harvard University’s endowment totaled approximately $57 billion USD and, as of 2025, had earned a ten-year average return of 9.6%. Its asset allocation includes nearly 40% in private equity and 30% in hedge funds, with only 14% in public equities and 5% in bonds.

Family offices are used by many ultra-high-net-worth families. The range of assets they manage can vary from approximately $200 million to many billions of dollars. In a recent review of U.S. family office asset allocations, the following results emerged.

U.S. Family Office Asset Allocation (2025)

Source: UBS Global Family Office Report 2025, showing U.S. family office average allocations to traditional (46%) and alternative (54%) asset classes.

Institutions and ultra-high-net-worth investors typically have both the capital and the patience required to invest in private assets. Over time, that has made a meaningful difference in the superior risk-adjusted returns they have achieved.

We have established that family offices with one billion dollars, endowments with tens of billions, and pension plans with hundreds of billions to invest are able to access the private capital opportunities they want.

The question then becomes how high-net-worth and ultra-high-net-worth investors, with far less capital, can participate in these markets in a sensible way. That is a question we have been asking ourselves as a firm for more than 25 years.

What are the attributes we need to see in private capital investment pools designed for our clients?

Answering that question properly requires a disciplined process. It begins with Stephen Covey’s Habit No. 2, “Begin with the end in mind.” From there, we objectively assess the current reality, much like the discussion above on private capital markets, and then build a plan to move from that reality toward the outcome we are trying to achieve.

The next step is to define the asset classes in which we want to provide access.

Private Fixed Income

This category includes real estate lending, which typically starts with first mortgages on residential or income-producing properties. These low-risk mortgages generally deliver yields comparable to, or slightly higher than, corporate bonds, with less default risk. Liquidity in these strategies is relatively high, as borrowers make regular monthly payments of principal and interest.

As risk tolerance increases, investors can move into second mortgages, land loans, or development financing. While yields can increase meaningfully in these areas, risk rises sharply and liquidity often declines, particularly during periods of market stress.

For investors seeking higher yields without taking on the elevated risk and reduced liquidity associated with development lending, private credit can be an attractive option within private fixed income.

The chart below, from Ares, a global asset manager with approximately $600 billion in assets under management, shows 20-year returns through mid-2024 across several asset classes. Notably, private credit returns are comparable to those of global developed public equities, but with roughly one-third of the risk. Public markets tend to be far more volatile, while private credit has historically offered a more stable return profile.

Private Markets Have Historically Offered Investors Better Risk-Adjusted Returns

Public vs. Private Risk and Return

Private Equity

Ares makes a compelling case for U.S. private equity markets using the data below, which shows the percentage of companies that remain private across both large-cap and middle-market segments. This trend has been reinforced by a sharp decline in the number of publicly traded companies in the U.S. since 1997.

Number and Market Cap of US Listed Companies 1980 - June 2024

Source: Bloomberg. Stock count from NASDAQ, New York Stock Exchange (NYSE), and New York Stock Exchange American.

The U.S. Economy (and Alpha) Is Increasingly Accessed Through Private Markets

A similar pattern can be seen in Canada. A December 2025 report from the Fraser Institute highlights that the number of publicly traded companies has fallen to 2,114 from 3,520 since 2008. The report attributes much of this decline to a challenging economic environment. While that may be a contributing factor, there is likely a broader explanation.

Being a public company has become increasingly complex and expensive. Reporting, regulatory, and compliance requirements create strong incentives for many businesses to remain private. In Canada, there are more than 1.1 million private employers, and that number continues to grow each year, according to Statistics Canada data from 2023.

At the same time, private equity and private debt markets now have access to substantial pools of capital. As a result, private companies no longer need to go public in order to achieve liquidity, fund growth, or create viable exit strategies for owners.

In both Canada and the United States, private companies account for a significant share of GDP. Investors who do not have some exposure to private capital markets are therefore missing participation in a large and growing portion of the overall economy.

Real Estate

A recent article from CRE Daily noted that the estimated value of global real estate is approaching $400 trillion USD.

Commercial real estate represents roughly $60 trillion of that total, while residential real estate accounts for close to 75%, or approximately $287 trillion USD. Much of the residential category, however, includes multi-family rental assets, which can be an attractive and relatively conservative investment. If we remove personal-use housing as an investable asset, the residual market would be similar in value to that of all public equity markets combined, estimated at $126 trillion USD. Other types of real estate investment options include farmland, timber, and infrastructure.

As of 2025, the eight largest Canadian pension plans, commonly referred to as the Maple 8, managed approximately $2.4 trillion CAD in assets. About 20% of those assets, or roughly $500 billion CAD, are invested in real estate and infrastructure.

Real estate has several attractive features for pension plans that must meet long-term retirement income obligations for millions of Canadians. Much of the return from both real estate and infrastructure is in the form of rental income. This income tends to rise over time in line with inflation and has low volatility.

Core: Putting It All Together

The image below outlines our process for combining strategic and tactical asset allocation, reflecting Aristotle’s observation that the whole is greater than the sum of its parts.

Since January 2000, we have tracked our results on a cumulative basis for our clients, net of all fees, and compared them with external benchmarks.

For most of the past 26 years, our Core Composite model has outperformed the indices referenced above. More recently, both the S&P 500 (in Canadian dollars) and the S&P/TSX have moved ahead as a result of a strong bull market in equities.

We believe that when mean reversion reasserts itself, the Core Composite will outperform and do so with significantly less volatility. Our primary objectives for clients are as follows:

- Earn an inflation-adjusted annual return of 4%. Inflation has averaged 2.14% from January 2000 through December 2025, which translates into a nominal return target of approximately 4.74% per year.

- We aim for roughly 50% of total returns to come from income in the form of rents, dividends, and interest. Currently, the yield of our Core Composite is just over 4%. This dramatically reduces the volatility of the portfolio.

Summary

This article focuses on two key principles that influence investor returns.

The first is the likelihood of mean reversion when asset classes experience returns that are meaningfully above or below their long-term averages. As of January 2026, most global public equity markets were at or near record highs and record valuations.

The opposite is true for other asset classes, such as real estate and infrastructure. Our view is that both will experience mean reversion, but in opposite directions.

The second principle is that strategic asset allocation is critical to building wealth and achieving consistent long-term returns. The world’s largest institutions and ultra-high-net-worth families have made this approach a cornerstone of their investment platforms.

For individual investors to replicate this model, they require access to open-ended and evergreen investment options in private capital markets. This is what our pools have been able to provide for our clients.

Want to go deeper? Tune into our companion podcast episode where we expand on this topic with additional context, commentary, and real‑world perspective.

Disclaimer

This material contains the current opinions of the author, and such opinions are subject to change without notice. This material is distributed for informational purposes only and is not intended to provide legal, accounting, tax or specific investment advice. Forecasts, estimates, and certain information contained herein are based upon proprietary research and should not be considered as investment advice or a recommendation of any particular security, strategy, or investment product. All investments contain risk and may gain or lose value. Please speak to your Nicola Wealth advisor for advice based on your unique circumstances. This is not a sales solicitation. This investment is intended for tax residents of Canada who are accredited investors. Residency restrictions apply. Please read the relevant documentation for additional details and important disclosure information, including terms of redemption and limited liquidity. Distribution Yield reflects the annualized fixed distribution rate that the Fund is expected to pay to unitholders, based on the Fund’s most recent declared distribution. Distributions are not guaranteed and may vary in amount and frequency over time. Duration is a measure of the sensitivity of a bond’s price to changes in interest rates. An increase in interest rates is associated with a decrease in bond prices, whereas a decrease in interest rates is linked to an increase in bond prices. The duration for the Nicola High Yield Bond Fund is an estimate based on best available information and is subject to change without notice. Sharpe ratio measures the risk-adjusted return, helping investors understand how much an investment compensates for the risk taken. It is calculated by dividing a fund return less cash (riskless) return by its risk standard deviation. Past performance is not indicative of future results. All investments contain risk and may gain or lose value. Returns are net of fund expenses charged to date. The Nicola Core Composite returns represent the total Canadian dollar returns of all fee paying portfolios with a Nicola Core mandate. The composite includes clients who are both fully discretionary and nondiscretionary. Historical net of fee composite performance returns are calculated using individual realized time-weighted client returns net of fees and is presented before tax. The Nicola Wealth inclusion policy is based on clients’ weights at calendar month end. The composite returns are asset-weighted based upon ending monthly market value. The Nicola Core mandate may change throughout time. Additional information regarding policies for calculating and reporting returns is available upon request. The composite returns presented represent past performance and is not a reliable indicator of future results, which may vary. Nicola Wealth Management Ltd. (Nicola Wealth) is registered as a Portfolio Manager, Exempt Market Dealer and Investment Fund Manager with the required securities commissions. Morningstar Canadian Neutral Balanced is a proprietary index developed by Morningstar Canada based on the CIFSC Fund categories (www.cifsc.org). This index includes funds which meet the following criteria: Funds in the Canadian Neutral Balanced category must invest at least 70% of total assets in a combination of equity securities domiciled in Canada and Canadian dollar denominated fixed income securities and between 40% and 60% of their total assets in equity securities. Comparisons of the historical performance of Nicola Wealth funds or models to the historical performance of indexes, mutual funds or other investment vehicles should only be undertaken with consideration of the differences that exist between the underlying investments that comprise the compared investment vehicles. Indexes may be primarily composed of a single asset type/asset class (i.e. 100% equities or 100% bonds) whereas Nicola Wealth funds may or may not contain a combination of exchange-traded equities, marketable bonds, private investments, other alternative investment classes and exempt products. When making any comparison of historical performance, these differences and their impact on the performance of each comparable should be taken into account. Nicola Wealth Management Ltd. (Nicola Wealth) is registered as a Portfolio Manager, Exempt Market Dealer and Investment Fund Manager with the required securities commissions.